3/30 Balancing Act

Phoenix's Market Deterioration Accelerates, Mortgage Rates Remain Stagnant, 1/3 Of Young Homebuyers Rely On Family Cash

This newsletter is 1,017 words and should take about 9 minutes to read.

Read last week’s newsletter here → "3/30 Emergency Press Conference"

The 1% of the world’s wealth has reached $44.6T. Sam Bankman-Fried was sentenced to 25 years in prison. P-Dilly was raided by the FBI for human trafficking. The NFL are changing the way kick-offs will be operated starting next season. Jaime Dimon had lunch with Kamala Harris. And Canada will cap mortgages for certain borrowers.

tl;dr

Phoenix’s inventory increased while demand decreased. This is the first time this inverse has happened in 2024. This is an indicator of a rapid market slowdown. Which is strange becasue spring is usually Arizona’s “busy season”.

The average mortgage rate is 6.91%

1/3 of young homebuyers say they plan to use their family’s money for a down payment on their house.

Phoenix

Supply has been gently increasing since the start of 2024 and has reached comfortably north of 17,000. This is still well below the long-term average but is the highest total we has seen in late March since 2019.

Re-sales have been suffering from strong competition from new homes and this source of supply is looking stronger than last year. In February there were 2,810 single-family home permits across Maricopa and Pinal counties which is the highest number since March 2022 and up 107% compared to February last year.

Multi-family permits for February were lower at 1,147 units, down 51% from a year ago. However multi-family permits are a very lumpy number that fluctuates wildly from month to month. It makes more sense to look at an annual running total. This stands at over 20,000 units, which is twice the level we regarded as normal until 2022.

Sellers should expect to be facing increased competition from the new home builders over the coming 12 months.

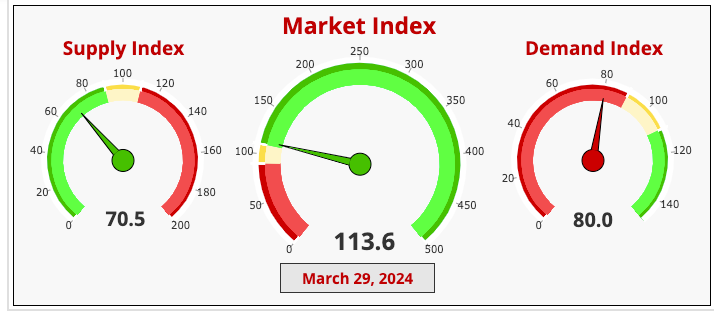

The Cromford Market Index is a gauge of Phoenix’s Supply and demand metrics. 100 is considered a balanced market. Anything higher than the 100-point benchmark is considered a seller’s market. Anything below 100 is considered a buyer’s market.

As of March 29th, 2024, the CMI has decreased to 113.6. Down 9 basis points from 7 days ago.

Supply has increased by 6 basis points and demand has decreased by 2 basis point.

This is the first week this year where supply has increased and demand decreased. This inverse will lead to the to an acceleration in market deterioration.

Rates

7-Day rate change: 0 basis points

YoY change: +31 basis points

Average interest rate: 6.91%

Mommy & daddy’s money

More than one third of young homebuyers which are Millennials and Gen Z combined plan to use money from family to fund their down payment.

Based on a February survey conducted by Qualtrics and fielded nationwide to 3k U.S. homeowners and renters.

Gen Z and millennial homebuyers are also getting help from family in other ways:

16% say they’ll use an inheritance to help cover their down payment

13% say they plan to live with their parents or other family members

Working to earn more money is still the most common way for young homebuyers to fund down payments:

60% say they’ll save money directly from paychecks

39% say they’ll work a second job

The point is pretty much all young American homebuyers need additional funds to put down money on a home. And those who don’t have family members both willing and able to provide financial assistance are at a significant disadvantage.

This comes after COVID’s zero interest rate environment caused all asset classes to skyrocket. Leaving families that were heavily invested to generate a much higher net-worth.

S&p 500 vibe check

US stocks rose yesterday with the S&P closing at a new record high and heading for its best Q1 since 2019

Mexican peso reached a 9-year high

Japanese yen dipped to a 34-year low against the dollar

Meme, tweet, & fact of the week

April also only had 29 days, but a 30th day was added when Julius Caesar established the Julian calendar.